Can two accounting principles be used in the same business?

2 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

6 min read

In a professional services organisation, hours and projects are the basis for customer invoicing rather than manufacturing or goods.

Typically, these organisations sell various services – consulting hours, courses, or standard services. Some customers purchase prepaid hours (like a ticket coupon), while others purchase entire projects on a fixed-price basis.

We see that many smaller consultancies often use the standard contracts on time & material or fixed price, but in some cases, using more complex contracts might be better for the bottom line.

This guide will review the most commonly used contract forms and best practices, especially for consultancies.

Maybe it will inspire you to make more comprehensive use of contracts depending on the projects and customers you enter into agreements with.

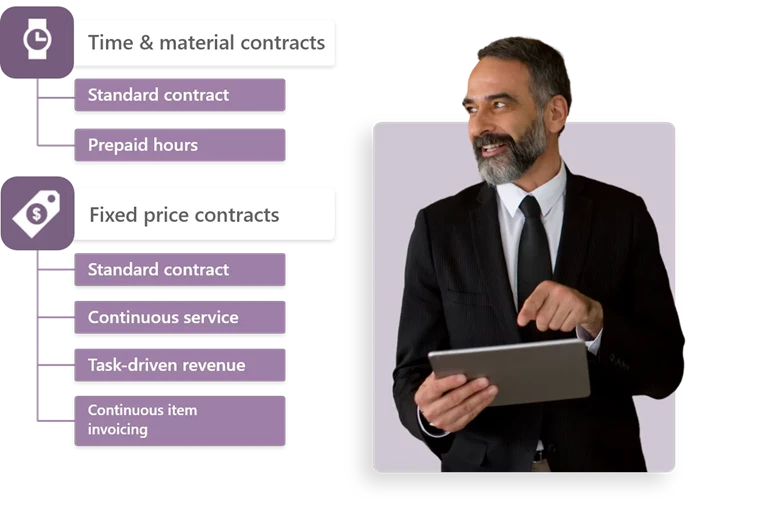

The contract types are divided into two main categories:

Each main type holds anomalies, for example, time and material at the maximum budget and special rules for revenue recognition at a fixed price.

This type of contract is for simple and very common contracts for which the customer is invoiced continuously based on time and materials spent. It takes its point of departure in hours x hourly rate.

You can define hourly rates for customers, employees or subtasks, and invoicing is based on consumption.

There are both pros and cons for using Time & material.

The contract type may cause uncertainty about what amount you can invoice in a given period, and if the projects have a shorter duration than expected, you will see this when invoicing.

On the other hand, you are sure to get paid for the hours spent, but you run a risk with fixed-price projects if the projects, e.g. are extended although the payment is the same.

The contract type prepaid hours is especially used within the IT industry. Prepaid hours is when the customer purchases a pool of hours at a discount.

The customer then spends some or all of these hours (like a voucher) on projects he needs carried out and then buys a new pool of hours if needed.

The cons of using this contract type can be:

Although these contracts indicate the use of hours, financially speaking it is just a prepayment which is depreciated as the debt to the customer is settled.

The advantage is that you can get a prepayment and secure an income. If you agree that one hour corresponds to one voucher, it is straightforward to control the prepaid hours. You may even be able to ask the customers for additional hours ahead of time.

This invoicing type is a variety of the standard Time and material – continuous payment. Large long-term projects use this type of contract, where you have requested payment for part of the total budget before and during project work but where the final consumption is to be invoiced upon project completion.

At the end of the project, a balance of what the customers have paid in advance and the total consumption of hours is made.

One example is a time and material contract with an agreed budget of DKK 100,000 for which the customer accepts an advance payment of DKK 50,000, an additional DKK 10,000 halfway through the project and the remaining amount upon completion.

As the contract is based on time and material, the remaining amount is the difference between the work cost and the DKK 60,000 paid, which is then invoiced before delivering the project.

The advantage of this invoicing type is that you still get paid per hour but have initial capital and invoicing does not have to wait until you have done the work.

The disadvantage may be that you have overestimated the project, so the customer ends up paying too much, which you will have to credit at the end of the project.

This type of invoicing is typically seen in industries with ongoing cooperation between customers and suppliers. Here, the supplier invoices the customer for a budgeted amount every period in advance – typically monthly or quarterly.

Once the period is over, the prepayment is offset against the value of the actual work performed during the period. The customer then receives an invoice including this balance and the prepayment for the coming period.

This type of invoicing is often used in consultancies providing ongoing and unspecified assistance for their clients.

Another type of fixed-price contract, the Continuous service contract, is based on well-defined periodic payments. The advantage is that you secure a regular income, which can be included in the budget for the agreed contract period. Please note that you must pay back the customer if work is done faster than you thought.

Both on-account invoicing types must be managed manually if you do not use a professional time tracking and automated project invoicing system.

Learn how to put the right price on your projects and take control of customer contracts:

Typical fixed-price contracts are based on a fixed price agreed upon with the customer and used for invoicing when the purchased service/product is delivered or during the project.

The first invoicing type is Invoicing based on a payment plan with revenue recognition per project, a so-called Fixed price standard contract.

This contract type is used for typical fixed-price deliveries, where the customer pays a fixed amount for delivery, for example, according to a multiple-payment plan.

What are the pros and cons of invoicing based on a payment plan with per-project revenue recognition?

For fixed-price projects, the supplier carries the risk of budget overruns, but conversely, the supplier can achieve high hourly rates and contribution margins through effective project management.

Selling every product or service at a fixed price can be tempting, requiring less administration and invoicing. On the other hand, it can be an unfortunate shortcut, as it poses increased challenges in managing accounts, work in progress and the bottom line in general.

The challenges peak at long-term fixed-price projects, where revenue recognition is expected to follow performance. In other words, there is a need to continuously make a so-called completion level assessment for calculating turnover.

For example, in the case of significant deliveries, many companies prefer to invoice the customer on an ongoing basis: 40% of the contract total in advance, 50% after the first significant delivery and 10% upon final delivery.

Some companies are particularly demanding regarding the level of detail in revenue recognition and invoicing. As such, viewing each project as a financial unit is insufficient.

This may be because every project task has its separate payment, which is released for invoicing as soon as it is finished. It may also be due to in-house procedures, revenue budgets (and bonuses) for individual departments, teams or employees.

Dividing a project into a clearly defined and intangible revenue framework might be prudent in these cases. This is particularly interesting if the delivery determines payments for the individual sections of a contract.

Example: a company offering monthly salary management based on the number of payslips processed and supply consultancy at a fixed monthly price. The easiest solution here is to group everything in one project and one contract while controlling the invoiced value for payslip processing, which only flows to work carried out on the payslip task.

By controlling the revenue recognition per subtasks (payslips and counselling), the company can always see the contribution margin on the different tasks within the same fixed-price contract. Is it through the administration of payslips or counselling you earn the most money?

This is the advanced management of fixed-price contracts compared to the "normal" standard agreement described earlier. Please consider if you must separate the value on the different subtasks.

Now, let's turn to the continuous contract types: Service contract (continuous contract) and Item invoicing (continuous contract).

Many IT, accountants and product-based companies supply services based on monthly, quarterly or annual contracts, i.e. subscriptions.

Customers are invoiced at a fixed monthly rate, regardless of the time spent completing the task. Invoicing these contracts is not a demanding job per se; it can be solved using one of many financial systems supporting subscription invoicing.

The main challenge is revenue; for a company measuring revenue based on departments, teams or employees, forecasting and revenue recognition need to consider that every period of the agreement cannot take in more than the invoiced value of the period as revenue.

In practice, many companies need to manually recognise revenue for work – a time-consuming and high-risk process. Also, the key figures are highly imprecise for the current accounting period, as the adaptation to periodic budgets is only performed in connection with bookkeeping.

Therefore, finding a system that takes its point of departure in invoicing and revenue recognition is essential to ensure you get the right picture of value creation.

The fixed-price contract with volume-based invoicing is an advanced variant of the fixed-price service contract.

These contracts are based on goods, not hours, despite these being consulting services.

Here are some examples of contract types with consulting invoiced as items:

In more complex cases, a direct external cost of the goods in question may be attached, e.g. a software license, etc., to be handled.

The disadvantage of this contract type is that it is challenging to manage for a consultancy since the number of items often varies monthly (e.g. the no. of payslips). This means the monthly budget for the work and direct costs also vary.

The advantage is that this type supports sales of other surrounding services, and the consultancies become less dependent on only selling hours.

I hope that my assessment of the contract types has made you smarter or inspired you to expand your contract invoicing in your company, depending on the services you offer.

2 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

5 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

6 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

3 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

8 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

6 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

5 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

5 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.

7 min read

What are the eight most commonly used contract and payment terms for consultancies? Best practices and tips to improve your bottom line now.