The invoicing process is the consultancy’s lifeblood

12 min read

2 min read

The consultants of a consultancy firm are the engines that keep the business running – and, as such, the core of the firm’s activities and earnings. That’s why all consultancy firms dream of employing consultants capable of invoicing all billable hours at the maximum hourly rate. In real life, however, this is rarely the case.

To achieve an impressive turnover, consultants and management alike need to stay current on the amount of value generated by the firm’s employees every hour and whether the hourly value is at risk from overrun.

For most consultancy firms, the consultants are free to prioritise their work and, to some extent, delivery. Consequently, granting consultants access to their own key figures can be monumentally significant in achieving results. The sequence of jobs, for instance, can significantly affect turnover, just as delivery impacts the hourly rate.

So why are only a minority of consultancy firms using structured and ongoing communication to present generated values and contribution margins to their consultants?

The answer is simple: collecting and presenting data on projects, finances and value generation before they’re in the system and before the project is finished is time-consuming, expensive and complex.

Financial management in small to medium-sized consultancy firms is often based on three principles:

This model is simple for financial controllers but often useless as a day-to-day tool for management and employees. It’s simply too unrefined and slow.

In other words, the financial system best suits the invoicing principle (the least time-consuming one). In contrast, the company is better off being managed according to the production principle, in which turnover on projects and for consultants is not defined by when invoicing is carried out but by when the work is put in.

So why not think outside the box and mix the principles? Run your financial system after the invoicing principle and your company after the production principle. Several of our customers have benefited from this model, in which ongoing reporting on finished work is based on the production principle using figures retrieved from TimeLog PSA.

To some accountants, this seems a ludicrous idea. After all, it will unbalance the system’s turnover, which is communicated externally, and the time registration and project management system, which is communicated internally.

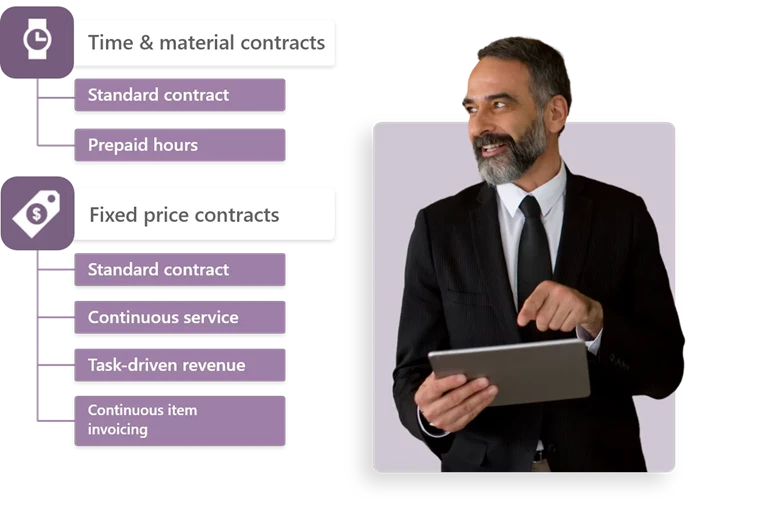

This drawback is offset, however, by each project manager, consultant and manager having constant access to the latest value generation figures from updated time registrations, regardless of whether your project is based on

The spread between generated value and invoiced value is simply ongoing work, which the auditor can access at the end of the financial year.

It couldn’t be simpler.