Why you should automate project invoicing

3 min read

We have recently talked about some of the biggest mistakes of project management, and one of them was inefficient invoicing management. For companies...

3 min read

Is manual bookkeeping putting a strain on your time and resources? There may be more efficient ways to divide those assets to support your business better.

Don't worry - our guide to the new Bookkeeping Act will help you quickly navigate the complexity of the legislation.

Implementing this new bookkeeping act is expected to improve your efficiency by streamlining the process and freeing up more time for you to focus on other tasks.

The Bookkeeping Act, which became effective on 24 May 2022, is a significant milestone in promoting the digitalization of bookkeeping and streamlining companies' reporting procedures to authorities.

The mandate for digital bookkeeping and digital bookkeeping systems will simplify recording purchases and sales, reconciling accounts with banks, and submitting annual accounts and VAT reports.

A "Business case" by PWC presented a proposal for a new bookkeeping law" published in 2022. It estimates that this initiative will provide Danish companies an annual administrative relief of DKK 2.9 billion, making it the most significant reduction of regulatory burdens ever implemented in Denmark's business community.

With the Bookkeeping Act in place, companies can easily comply with regulations, ensuring greater security for storing their accounting material, particularly in cases where cybercrime may occur.

Please note that the above timetable only concerns the requirements for standard digital accounting systems.

The requirements for customised accounting systems will also only enter into force later. The requirements for these will be prepared in the first half of 2023.

The Danish Business Authority will inform about requirements and dates of entry into force on this page as they become available. They will also update the page with information about deadlines.

The Danish Bookkeeping Act and the Executive Order on requirements set three basic requirements for standard digital bookkeeping systems:

Bookkeeping needs to be organised and carried out considering the complexity of your business, the number of transactions and the economic volume of transactions. This means that, in practice, how each company should keep its accounts can vary greatly.

In your organisation, you must establish and continuously maintain a satisfactory and secure accounting environment. This means, among other things, that you must install the internal controls and procedures necessary to ensure.

The accounting environment's organisation and performance should consider the business's complexity, the number of transactions, and the economic size of the transactions. However, there are also general requirements for the accounting environment that do not depend on the complexity of the organisation, the number of transactions, and the economic size of the transactions. The general requirements are:

3 min read

We have recently talked about some of the biggest mistakes of project management, and one of them was inefficient invoicing management. For companies...

5 min read

Do you throw away revenue and profit to inflation because you don't index your hourly rates? We all know the feeling that everything was...

8 min read

You probably know that a business process is a chain of activities that are repeated. You, as others, may see visions of documentation and...

5 min read

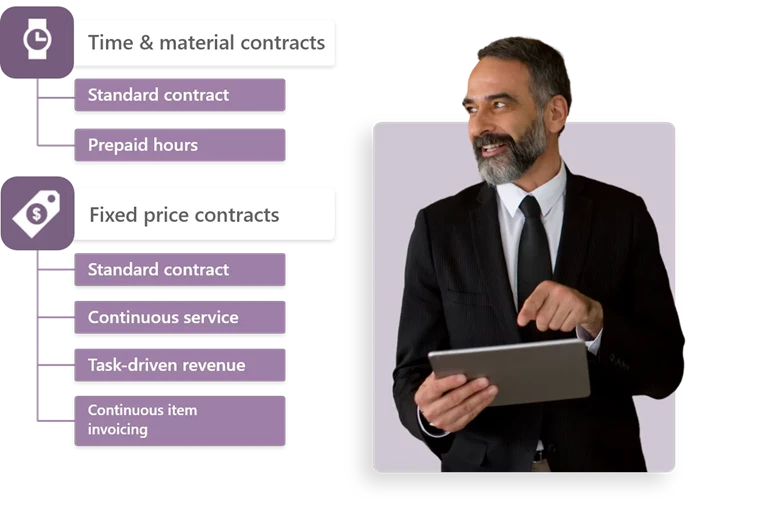

Consultancies typically work for numerous clients either on a retainer, fixed price project, or time and material, invoicing the clients for...

2 min read

The consultants of a consultancy firm are the engines that keep the business running – and as such, the very core of the firm’s activities and...

6 min read

What is the problem with receiving personal information via e-mail? Before the new GDPR rules took effect on 25 May 2018, it was common...

8 min read

In a professional services organisation, hours and projects are the basis for customer invoicing rather than manufacturing or goods. ...

6 min read

Is the role of project manager brand new to you? Or maybe you are wondering what type of project manager you want to be. Or have you been...

15 min read

As a project manager, you constantly need to balance stakeholders' and customers' interests while executing on time and within scope along...